Prevent Account Takeover Fraud With Account Change Risk Insights

Flag Suspicious Activity With a Comprehensive Identity Solution

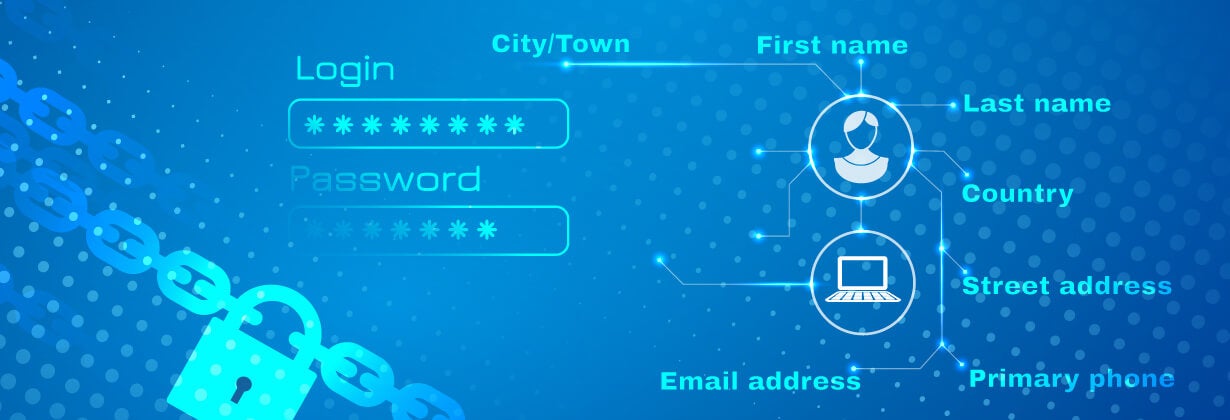

A consumer just changed the email address associated with his account in your account management system. Now you have a difficult question to answer. Was it the actual customer who initiated the request? Or could it have been a criminal who’s taken over their account? With account takeover fraud becoming more pervasive and more costly, it’s a question you’ll want to answer correctly.

A Three-Step Process

Account takeover fraud is a form of identity theft. It works through a series of small steps:

- A fraudster gains access to victims’ accounts.

- Then, makes non-monetary changes to account details such as:

- Modifies personally identifiable information (PII)

- Requests a new card

- Adds an authorized user

- Changes the password

- Once one of these seemingly insignificant tasks is successful, the ability to carry out numerous unauthorized transactions is wide open—all of which will ultimately result in a financial loss and often the loss of the victimized customer relationship.

Types of Vulnerable Accounts

Further complicating matters is that activities typically associated with account takeover fraud—changing the email, phone number or password associated with an account—occur many times a day. Fortunately, the vast majority of these customer-initiated account management actions are legitimate. But how can you tell when they’re not?

You need the right processes and tools in place to differentiate between real customers and fraudsters. When you can’t identify fraudsters in real time, the losses can quickly mount.

Why Account Takeover Is So Insidious

When account takeover attempts are successful, the cost for the customer can be monetary as well as lost time and frustration when they try to undo the damage that’s been done. For the organization that didn’t or couldn’t stop the compromise of the account, the losses can extend far beyond the costs tied to the individual account.

Account takeover strains customer relationships. And when it happens frequently, it can result in long-term damage to a company’s brand.

Account Takeover Fraud Is Far Reaching

When fraudsters steal a credit card, they’ve stolen one relationship. With account takeover, criminals have the potential to infiltrate multiple relationships of their victims.

They can use stolen account information—usernames, passwords, email and mailing addresses, bank account routing information and Social Security numbers—to forge a full-blown attack on a person’s identity.

Fraudsters move quickly to use the data gathered from one account takeover scheme or data breach to take over additional accounts at other companies.

Even worse, criminals often collaborate and sell compromised identities to the highest bidder, resulting in further damage to the consumer’s accounts and identity.

Ensuring Security With Minimal Friction for Customers

When customers experience account takeover, they often hold the company responsible for lenient security that allowed the fraudster to access their account. At the same time, customers are easily frustrated when small requested changes result in excess scrutiny and become a hassle.

Organizations must find a balance between implementing adequate security and providing a seamless customer experience. How can companies stay ahead of fraudsters while minimizing customer friction on the millions of benign account management activities that occur daily?

Account Takeover Fraud Requires a Comprehensive Solution

Your business cannot afford to alienate and lose customers due to restrictive account management access or account takeover. Combating this type of fraud requires a comprehensive, real-time understanding of normal and abnormal account maintenance activity across your organization’s channels and product areas.

A cross-industry perspective can help flag suspicious activity before losses occur. This is where the LexisNexis® Risk Solutions proprietary repository of identity information comes in.

With more than 100 million new identity elements coming in every day, we can help you determine whether a change in account information is likely coming from the account owner or is the first step in an account takeover.

Prevent Account Takeover Fraud Through Insight Into Critical Risk Factors

LexisNexis Risk Solutions has the ability to assess the account takeover risk associated with changes to account information and looks for a range of risk indicators, including:

- Has the account holder made similar changes at other organizations?

- Holistically, does the full set of requested account changes match a pattern of account takeover?

- For PII changes, does the new information being added to the account (i.e. new address or phone) have a history of high-risk behavior?

- For PII changes, does the comparison of old and new information reveal a high-risk behavior?

These insights drive an evaluation which allows legitimate customers to change their information with minimal hassle while stopping fraudsters in their tracks by detecting truly high-risk changes.

Contact Sales to learn more about solutions for account takeover fraud.

Have Sales Contact Me

This article is for educational purposes only and does not guarantee the functionality or features of LexisNexis products identified. LexisNexis does not warrant this article is complete or error-free.